Atal Pension Yojana 2024

Atal Pension Yojana (APY) is a retirement savings scheme in the 2015-16 budget for people aged 18-40 with a savings account, not paying income tax. It aims to help those in the unorganized sector save for retirement. APY focuses on providing retirement benefits to economically disadvantaged individuals, especially those in the unorganized sector. Let’s check the details about Atal Pension Yojana 2024.

Overview Table Of Atal Pension Yojana

| Aspects | Details |

| Scheme Name | Atal Pension Yojana (APY) |

| Announced On | 2015-16 Budget |

| Objective | To provide retirement benefits to economically disadvantaged individuals, especially those in the unorganized sector. |

| Eligibility | Citizens aged 18-40 without any existing pension scheme and not paying income tax. |

| Administered By | Pension Fund Regulatory and Development Authority (PFRDA) under the National Pension System (NPS). |

| Minimum Pension | Rs. 1000 to Rs. 5000 per month guaranteed upon reaching the age of 60. |

| Contribution Period | Until the subscriber reaches 60 years of age. |

| Exit Before 60 | Subscribers exiting before 60 years can get a refund of their contributions along with net actual accrued income earned, after deducting account maintenance charges. |

| Documents Required | KYC details fetched from the bank/post office savings account. |

What Is Atal Pension Scheme?

The Indian Government is committed to ensuring financial security for elderly workers and helping them save for retirement. To address the longevity risks faced by those in the unorganized sector and promote voluntary retirement savings, the Government launched the Atal Pension Yojana (APY) in the 2015-16 budget.

This scheme is designed for all citizens working in the unorganized sector. It is overseen by the Pension Fund Regulatory and Development Authority (PFRDA) within the framework of the National Pension System (NPS). The primary focus of the scheme is on providing retirement benefits to economically disadvantaged individuals, particularly those working in the unorganized sector.

अटल पेंशन योजना

अटल पेंशन योजना (एपीवाई) भारत सरकार की एक महत्वपूर्ण पेंशन योजना है जो 18 से 40 वर्ष की आयु समूह के लोगों के लिए विकसित की गई है। यह योजना उन लोगों के लिए है जो किसी भी पेंशन योजना के तहत नहीं आते हैं और जो आयकर करदाता नहीं हैं। यह योजना वृद्ध अधिकारी को वित्तीय सुरक्षा प्रदान करने और उन्हें पेंशन के लिए बचत करने की शक्ति प्रदान करने का लक्ष्य रखती है।

अटल पेंशन योजना का प्रमुख उद्देश्य उन असंगठित क्षेत्र के श्रमिकों को दीर्घावधि जीवन के लिए निवेश करने के लिए प्रोत्साहित करना है। यह योजना अप्रैल 2015 में शुरू की गई थी और इसका प्रबंधन पेंशन फंड नियामक और विकास प्राधिकरण (पीएफआरडीए) द्वारा किया जाता है। एनपीएस परिप्रेक्ष्य में।

अटल पेंशन योजना के तहत, सदस्यों को विभिन्न आयुवर्गों के अनुसार निर्धारित पेंशन राशि के लिए प्रतिमाह योगदान देने की सुविधा होती है। यह योजना वित्तीय सुरक्षा को सुनिश्चित करने के लिए एक महत्वपूर्ण कदम है, खासकर उन लोगों के लिए जो स्वतंत्र रूप से पेंशन के लिए बचत करना चाहते हैं।

Atal Pension Yojana Features

- The Atal Pension Yojana (APY) guarantees a minimum monthly pension for subscribers, ranging from Rs. 1000 to Rs. 5000 per month.

- The Government of India (GoI) ensures the minimum pension benefit for subscribers.

- The GoI will co-contribute 50% of the subscriber’s contribution or Rs. 1000 per annum, whichever is lower. This co-contribution is available for individuals not covered by any Statutory Social Security Schemes and who are not income tax payers.

- The GoI will co-contribute to each eligible subscriber for a period of 5 years i.e., from Financial Year 2015-16 to 2019-20, who join the NPS between the period 1st June, 2015 and 31st March, 2016 and who are not members of any statutory social security scheme and who are not income tax payers.

- The maximum benefit of government co-contribution under APY for any subscriber, including migrated Swavalamban beneficiaries, is limited to 5 years.

- All bank account holders are eligible to join APY.

Atal Pension Yojana Benefits

Upon reaching the age of 60, subscribers to the Atal Pension Yojana (APY) will receive the following benefits:

(i) Guaranteed Minimum Pension Amount: Each subscriber will receive a guaranteed minimum pension of Rs. 1000/-, Rs. 2000/-, Rs. 3000/-, Rs. 4000/-, or Rs. 5000/- per month until death.

(ii) Guaranteed Minimum Pension Amount to the Spouse: After the subscriber’s death, the spouse will receive the same pension amount until their demise.

(iii) Return of Pension Wealth to the Nominee: Upon the demise of both the subscriber and the spouse, the nominee will receive the accumulated pension wealth until the subscriber’s age of 60 years.

Contributions to APY are eligible for tax benefits under section 80CCD(1), similar to the National Pension System (NPS).

Voluntary Exit (Exit Before 60 Years of Age):

If the subscriber exits before the age of 60, they will be refunded only their contributions to APY along with the net actual accrued income earned, after deducting account maintenance charges.

However, subscribers who joined before March 31, 2016, and received Government Co-Contribution will not receive the same or the accrued income earned thereon.

In Case of Death Before 60 Years:

Option 1: The spouse can continue contributing to the subscriber’s APY account until the subscriber would have turned 60. The spouse will receive the same pension amount until their demise. This is in addition to any existing APY account and pension amount in the spouse’s name.

Option 2: The entire accumulated pension amount under APY will be returned to the spouse or nominee.

Atal Pension Yojana Eligibility

- The minimum age for joining APY is 18 years, and the maximum age is 40 years.

- Pension starts and exit age is set at 60 years.

- Subscribers’ contributions to APY are deducted automatically from their savings bank accounts on a monthly, quarterly, or half-yearly basis.

- Contributions are mandatory from enrollment until the subscriber reaches the age of 60.

APY Subscriber’s Contribution Chart

| Age of Entry | Years of Contribution | Monthly pension of Rs. 1000 | Monthly pension of Rs. 2000 | Monthly pension of Rs. 3000 | Monthly pension of Rs. 4000 | Monthly pension of Rs. 5000 |

| 18 | 42 | 42 | 84 | 126 | 168 | 210 |

| 19 | 41 | 46 | 92 | 138 | 183 | 228 |

| 20 | 40 | 50 | 100 | 150 | 198 | 248 |

| 21 | 39 | 54 | 108 | 162 | 215 | 269 |

| 22 | 38 | 59 | 117 | 177 | 234 | 292 |

| 23 | 37 | 64 | 127 | 192 | 254 | 318 |

| 24 | 36 | 70 | 139 | 208 | 277 | 346 |

| 25 | 35 | 76 | 151 | 226 | 301 | 376 |

| 26 | 34 | 82 | 164 | 246 | 327 | 409 |

| 27 | 33 | 90 | 178 | 268 | 356 | 446 |

| 28 | 32 | 97 | 194 | 292 | 388 | 485 |

| 29 | 31 | 106 | 212 | 318 | 423 | 529 |

| 30 | 30 | 116 | 231 | 347 | 462 | 577 |

| 31 | 29 | 126 | 252 | 379 | 504 | 630 |

| 32 | 28 | 138 | 276 | 414 | 551 | 689 |

| 33 | 27 | 151 | 302 | 453 | 602 | 752 |

| 34 | 26 | 165 | 330 | 495 | 659 | 824 |

| 35 | 25 | 181 | 362 | 543 | 722 | 902 |

| 36 | 24 | 198 | 396 | 594 | 792 | 990 |

| 37 | 23 | 218 | 436 | 654 | 870 | 1087 |

| 38 | 22 | 240 | 480 | 720 | 957 | 1196 |

| 39 | 21 | 264 | 528 | 792 | 1054 | 1318 |

| 40 | 20 | 291 | 582 | 873 | 1164 | 1454 |

Atal Pension Yojana Apply Online

Process 1:

- Open an APY account online using Net banking.

- Log in to internet banking and find APY on the dashboard.

- Fill basic and nominee details.

- Consent for auto debit of premium and submit the form.

Process 2:

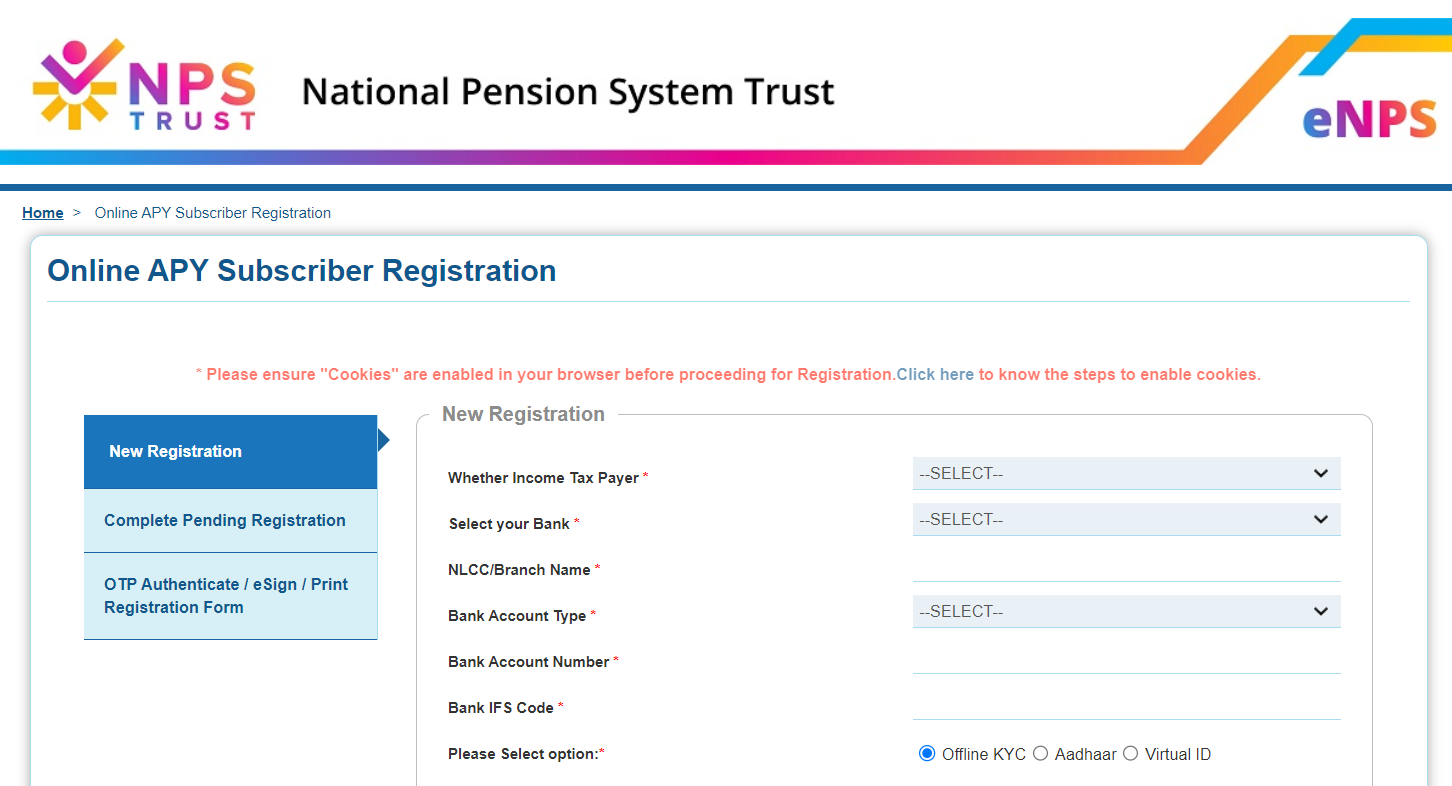

- Visit the website “https://enps.nsdl.com/eNPS/NationalPensionSystem.html”.

- Select “Atal Pension Yojana” and then “APY Registration”.

- Fill basic details and choose KYC method: Offline KYC, Aadhaar, or Virtual ID.

- Generate an acknowledgement number after filling basic details.

- Specify personal details and desired pension amount after 60 years, along with contribution frequency.

- Confirm personal details and fill nominee details.

- Citizen is redirected to NSDL website for eSign.

- Complete Aadhaar OTP verification to complete the registration.

APY Subscriber Registration Process

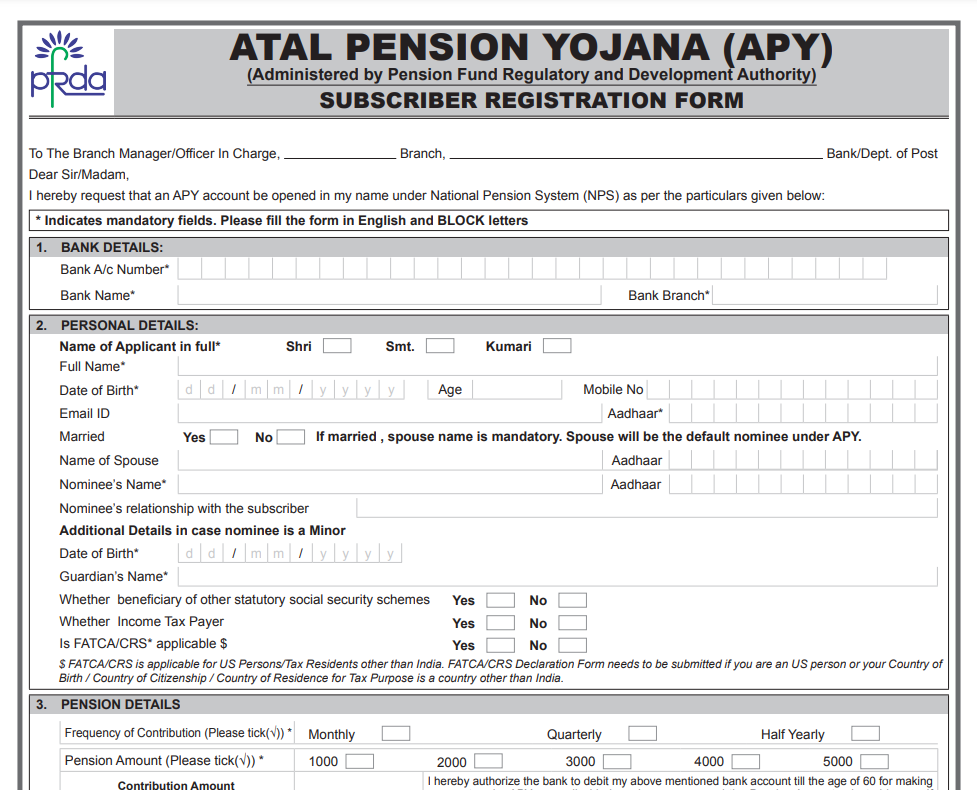

Individuals can visit their nearest bank branch or post office, where they hold a savings bank account, to submit the Atal Pension Yojana registration form and open an APY account.

Atal Pension Yojana Documents Required

KYC Details are fetched from the bank/post office savings account.

Conclusion

The Atal Pension Yojana (APY) has been crucial in ensuring financial security, especially for those in the unorganized sector. Since its start in 2015-16, APY has helped people aged 18-40 save for retirement with guaranteed pensions and government support.

Managed by the Pension Fund Regulatory and Development Authority (PFRDA) under the National Pension System (NPS), APY addresses the risks of long lives and promotes saving for retirement. It’s easy to join, even online, making it accessible to many.

Frequently Asked Questions

Ans: APY is a retirement savings scheme for people aged 18-40, aimed at providing retirement benefits to economically disadvantaged individuals, especially those in the unorganized sector.

Ans: tal Pension Yojana is administered by the Pension Fund Regulatory and Development Authority (PFRDA) under the National Pension System (NPS).

Ans: Benefits include guaranteed minimum monthly pension upon reaching 60, co-contribution from the Government of India, and tax benefits under section 80CCD(1).

Ans: There are two ways to apply: through net banking or by visiting the website “https://enps.nsdl.com/eNPS/NationalPensionSystem.html” and following the APY registration process provided in this article.

Ans: The minimum monthly pension amount ranges from Rs. 1000 to Rs. 5000, depending on the contributions and the age at which the subscriber joins the scheme. There’s also flexibility for subscribers to choose their pension amount within this range.

- GA Questions Asked In SBI PO Mains 2025, 5th May Analysis

- Pradhan Mantri Suraksha Bima Yojana 2024 Overview & Benefits

- Central Government Schemes 2024, List of Schemes under Every Ministries

- Pradhan Mantri Swasthya Suraksha Yojana (PMSSY) 2024

- Pradhan Mantri Gramodaya Yojana 2024 Features & Benefits

- Pradhan Mantri Van Dhan Yojana 2024, Features, Components & Stages