Letters of Credit for JAIIB: ‘Letters of Credit’ is a part of Unit-7 of Paper 3 for JAIIB. It comes under the Legal and Regulatory Aspects of Banking. For the IIBF JAIIB certification, it is necessary to score a minimum of 45 marks on each paper. Hence, candidates should learn each topic as well as possible, especially the high-weightage ones. This blog will provide all information on ‘Letters of Credit’ for JAIIB exam. This includes the definition, classification, documents, advantages, and disadvantages. Candidates will also be able to download the free PDF format of these notes in this blog. We hope these concise and thorough notes will help make your JAIIB preparation smoother.

Letters of Credit for JAIIB: Overview

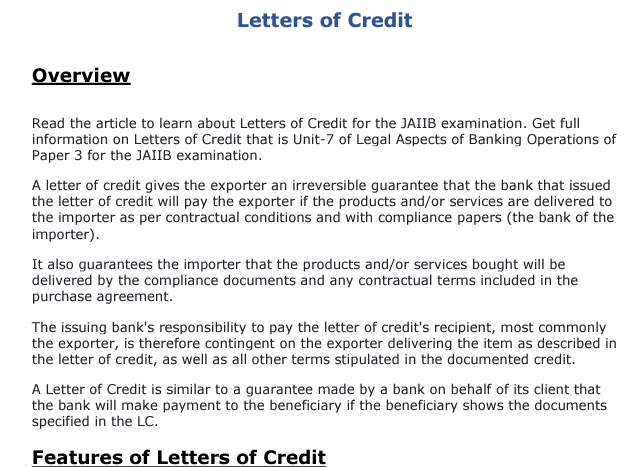

A bank is the issuing authority of a letter of credit. The bank addresses this letter to the exporter and gives them an irreversible guarantee that the bank will pay the exporter if the exporter delivers the to the importer as per contractual conditions and with compliance papers

The bank also guarantees the importer that the products and/or services they bought will be delivered by the exporter with compliance documents and any contractual terms included in the purchase agreement.

The issuing bank’s responsibility to pay the letter of credit’s recipient, most commonly the exporter, is therefore contingent on the exporter delivering the item as described in the letter of credit, as well as all other terms stipulated in the documented credit.

A Letter of Credit is similar to a guarantee made by a bank on behalf of its client that the bank will make payment to the beneficiary if the beneficiary shows the documents specified in the LC.

Letters of Credit for JAIIB

Features of Letters of Credit

- Revocability: Revocable or irrevocable letters of credit are available. It is not possible to verify a revocable letter of credit and the obligation to pay can be canceled at any moment. In an irreversible letter of credit, all parties have equal power; no one can amend or modify it without the unanimous permission of all parties.

- Negotiability: A letter of credit is a commercial agreement in which, at the parties’ discretion, the conditions can be amended or modified. A letter of credit must include an absolute guarantee to pay on demand or at a certain point in time to be negotiable.

- Sight and Time Drafts: The bank will only pay the recipient when the letter of credit matures if they produce all the relevant draughts and documentation to the issuing bank.

- Transfer and Assignment: The beneficiary has the authority to transfer this type of letter of credit. The LC will stay in force regardless of how many times the beneficiary assigns/transfers it.

Parties to a Letter of Credit

- Applicant-Buyer-Importer-Opener: This is the individual who applies for a Letter of Credit with the bank. Mr Srivastav & Co. is an example.

- Issuing Bank: An issuing bank is a bank that opens the Letter of Credit at the request of the applicant/buyer. Bank of Baroda, for example.

- Beneficiary-Exporter-Seller: The individual who is eligible for a Letter of Credit benefit. Ms. Jha & Co. is an example.

- Advising Bank / Notifying Bank: The bank in the Beneficiary/Exporters Country that advises the beneficiary of the letter of credit. The UK Bank, for example.

- Negotiating Bank: The bank that negotiates the bills in the beneficiary/exporter country (i.e., makes payments on the bills drawn by the seller and accepts the documents.) The Negotiating Bank, also known as the Nominated Bank / Paying Bank, is the bank specified in the LC. If the LC does not identify a bank, however, any bank can act as the negotiating bank.

- Confirming Bank: The advising bank’s main need is to notify the beneficiary of the credit. However, if the advising bank confirms the credit in addition to advising it, the advising bank becomes the confirming bank.

- Reimbursing Bank: The Issuing Bank appoints this bank to compensate the Negotiating, Paying, or Confirming Bank.

Types of Letters of Credit

- Acceptance Credit: Ordinary Letters of Credit are often sight credits, which require quick payment of bills drawn by the beneficiary. Acceptance Credit or Time Credit are letters of credit from which usance bills can be drawn.

- Revocable Credit: The issuing bank can terminate or change a revocable credit without prior notification to the beneficiary. However, the issuing bank has to compensate the negotiating bank if it has taken any action on the credit before receiving the notification of amendment/ cancellation.

- Irrevocable Credit: No one can alter this type of credit without the beneficiary’s approval.

- Confirmed Credit: If a bank that advises the credit to the recipient adds its confirmation to the credit, it is a confirmed credit. The only credit that is irreversible can be confirmed. With and without recourse credits: When a beneficiary draws a bill under an LC, he is responsible if the drawee fails to pay. This legislation is known as recourse LCs. The recipient can avoid obligation by adding the phrase “without recourse” to the bill.

- Transferable Credits: As a result, the beneficiary’s rights under an LC cannot be transferred. A transferable credit allows the recipient to assign his rights to third parties. An LC is not transferrable unless indicated.

- Back-To-Back Credits: The beneficiary who receives an LC utilizes it to acquire another credit from his (beneficiary’s) bank in favor of the supplier. Three banks are active in this sort of LC. (The issuing bank, the advising bank, and the third bank that provided an ancillary credit against the security of the initial credit.)

Anticipatory Letter of Credit

- Red Clause Letter of credit: In a regular LC transaction, the beneficiary avail payment after delivering the documentation and invoices issued under the LC to the negotiating bank. However, in some cases, the recipient can get a price advance. These credits include a “Red Clause,” which allows an intermediate bank to advance funds to the recipient before shipping.

- Green Clause Letter Of Credits: This is an improvement on the “Red Clause.” This sort of LC not only allows for pre-shipment advances but also for exporter advances to cover storage at the port of shipment. Anticipatory Credits are the Red Clause and Green Clause credits.

- Revolving Letter of Credit: Although the amount of credit cannot change, it can be renewed as soon as the previous payments are paid.

Documents Under Letter of Credit

- Insurance Document

- Invoice

- Bills of Lading

- Bills of Exchange

- Post Parcel Receipt and Courier Receipt

- Transport Documents

- Airway Bill

- Other Documents: Certificate of Weight or quality or analysis, Certificate of origin, Health authorities certificate etc.

The complexity and level of security for the transaction that the two parties require determines the documentation a letter of credit needs. Risks associated with transactions can be payment security, security and transparency regarding the goods’ description, security regarding Customs clearance, transportation process and timely delivery. One key component of the acceptance/endorsement procedure for letters of credit, particularly for the exporter’s bank, is the verification of document conformity.

The banking commission of the international chamber of commerce (ICC), which also provides arbitration services, regularly standardizes the legal terms of fundamental letters of credit. Documented letters of credit are one of the safest kinds of financing since they have solid and well-defined collateral and extensive paperwork. Commercial laws across the world accept such documents and collateral, and they are subject to arbitration in the event of default or other issues impacting the transaction.

Implementation Guidance

The International Chamber of Commerce (ICC) has created a uniform documentary credit application form. It also published the Uniform Customs & Practices for Document Credit. The ICC has made the rights and duties of purchasers, sellers, and participating institutions in international letters of credit transactions available in great detail in their publications.

UCPDC 600: Uniform Customers and Practices for Documentary Credits

On October 25, 2006, the ICC Banking Commission adopted UCP 600, ICC’s new documentary credit policy. UCP 600, which took effect on July 1, 2007, includes substantial amendments, such as:

- The UCP 500 reduced the number of articles from 49 to 39.

- The rules are now more precise and clearer, thanks to new entries on “Definitions” and “Interpretations.”

- The word “reasonable time” is now a definite timeframe of five banking days for acceptance or denial of papers.

- Deferred payment credits can now be discounted thanks to new regulations.

- Negotiation is best described as the “buying” of document draughts.

The Process

The following is the detailed process of acquiring a letter of credit:

- Step 1: The buyer accepts the seller’s offer to acquire items. The buyer and seller use a purchase order, a formal contract, an accepted Pro-forma invoice to create this agreement. An agreement is reached on the products to be acquired, the delivery, insurance, and the mode of payment. In this scenario, the agreement calls for payment via a letter of credit.

- Step 2: The buyer signs the bank’s letter of credit application form to apply for a letter of credit.

- Step 3: The issuing bank issues the real letter of credit instrument and delivers it to the seller after approving the application (beneficiary).

- Step 4: The vendor ships the products to the customer after receiving a payment guarantee from the issuing bank.

- Step 5: The seller prepares and provides the paperwork required by the letter of credit to the issuing bank.

- Step 6: The issuing bank examines the documents. The issuing bank pays the seller if the papers meet the letter of credit’s requirements.

- Step 7: The issuing bank collects payment from the application (buyer) in line with the letter of credit agreement’s provisions and sends the paperwork to the applicant.

- Step 8: The applicant picks up the product from the carrier with the paperwork, finishing the letter of the credit cycle.

Letter of Credit: Advantages

Letters of Credit have a variety of advantages over other means of conducting international commerce transactions. Some of the more important ones are as follows:

- It allows trading partners to transact with and communicate with new people, as well as build new commercial partnerships.

- It assists them in fast extending and broadening their business into new geographical regions.

- A letter of credit is extremely efficient and reliable.

- Both trade partners can stipulate terms and conditions based on their needs and desires. They can then agree on an exclusive set of provisions.

- A letter of credit frees the issuing bank from the responsibilities of the trade partners and any disputes that may arise as a result of such commitments.

- It transfers the exporter’s or buyer’s creditworthiness to the issuing bank. The importer can do an unlimited number of transactions at the same time. This is possible if they are supported by a well-established larger institution.

- A letter of credit protects the exporter if the importer goes bankrupt. Because the seller’s creditworthiness has been shifted to the issuing bank, the bank must pay the amount specified in the letter of credit. As a result, a letter of credit distinguishes the exporter from the importer’s firm.

- A letter of credit is simple to use.

- The seller must present confirmation of material kind and amount, as well as papers supporting his assertion that they have transported the items. The papers will be verified and evaluated by the advising bank according to the initial terms & conditions.

- If there is a disagreement between the trade partners, the exporter might withdraw the funds and settle the problem in court later.

- The vendor cannot withhold payment from the buyer by raising issues about the quality of the items. The bank simply needs to view the documentation.

- The exporter can employ pre-shipment financing against a letter of credit. This will assist him in filling any financing gaps that may exist.

Letters of Credit: Disadvantages

As with every financial instrument, this one includes drawbacks as well as perks, which are as follows:

- It raises the cost of running the business since banks charge a fee for their services.

- A letter of credit is subject to complicated regulating requirements. This may provide a loophole to take advantage of the applicant.

- A letter of credit warns the importer of major fraud risk.

- The bank will pay the exporter after meticulously reviewing the shipping documentation, not the actual quality of the items shown. There may be disputes and disagreements between parties if the quality differs from what they agreed upon.

- A letter of credit entails risk as well.

- A letter of credit has an expiry date. The bearer/beneficiary must use it before that date, which is the most significant negative since it creates a time constraint.

- A letter of credit entails payment risk. If the bank assures the payment, which increases the cost of the LC, this risk can be avoided.

- Issuers frequently handle LCs as though they were loans.

- Other less expensive forums include a bond, insurance, documented collection, open account sales, and a guarantee.

Letters of Credit for JAIIB: E-Book Sneak Peek

Take a look at what you’ll find in the free PDF of Letters of Credit e-book:

E-Book Download

Steps to Download Free E-Book

Step 1: Click on the download link. You will be redirected to Oliveboard’s FREE E-Books Page.

Step 2: Create a free Oliveboard account or login using your existing Oliveboard account details

Step 3: Download the book by clicking on the link presented on the page.

Letters of Credit for JAIIB: Conclusion

Exporters should keep in mind the importance of submitting papers in full accordance with the terms & conditions of the LC. Any breach of the LC might result in non-payment, late payment, or payment disputes. Hope this article provides you with a thorough grasp of the JAIIB exam. Please reach out to us for further queries.

Letters of Credit for JAIIB: Frequently Asked Questions

It would be entirely dependent on future events. For example, if a buyer is unable to make a payment to the bank, the bank must absorb the expense and arrange it on the buyer’s behalf.

A letter of credit is a negotiable instrument. This is because the bank deals with the paperwork rather than the products. With the consent of the parties, the transaction can be transferred.

- 1000 Vocabs PDF for Bank and Insurance Exams, LIVE Quiz

- JAIIB 2026 Previous Year Papers, Download Free PDF

- RRB NTPC Undergraduate Syllabus 2026, Check CBT 1 & 2 Exam Pattern

- RRB NTPC Graduate Syllabus 2026, Check CBT 1 & 2 Exam Pattern

- Practice Reading Comprehension Quiz 08, Attempt FREE

Hi, I’m Tripti, a senior content writer at Oliveboard, where I manage blog content along with community engagement across platforms like Telegram and WhatsApp. With 3+ years of experience in content and SEO optimization related to banking exams, I have led content for popular exams like SSC, banking, railway, and state exams.