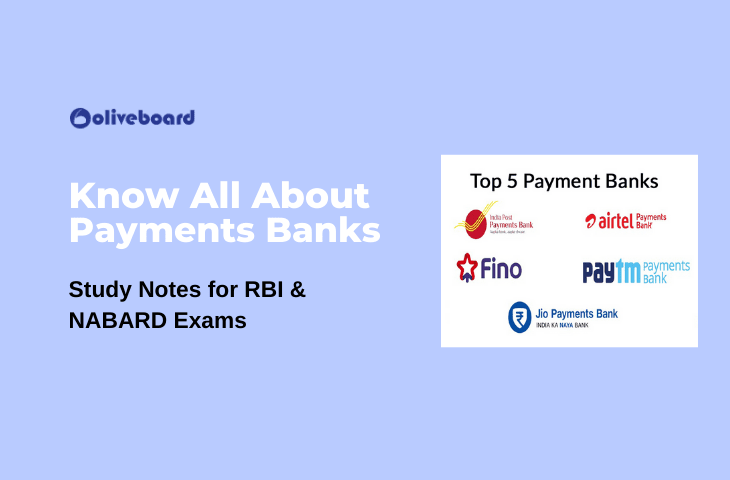

You must have heard about the payments banks in news for sure. Many of you might also have accounts in the payments banks. But are you really aware, what exactly payments banks are? Here in this article, we will get down to the nitty-gritty of payments banks in India and their scope. This knowledge can you answer questions in various bank & government exams like RBI Grade B, NABARD Grade A, SBI PO, IBPS PO etc. Let us get started.

I. Know All About Payments Banks in India

» What are Payment Banks?

- A payments bank is like any other bank, but operating on a smaller or restricted scale.

- Payments banks are registered as a public limited company under the Companies Act, 2013, and licensed under Section 22 of the Banking Regulation Act, 1949.

- The minimum paid-up equity capital of the payments bank shall be Rs. 100 crore.

- The promoters of the payments bank should hold at least 40% of its paid-up equity capital for the first five years from the commencement of its business.

» Scope of Activities of Payments Banks in India

- Acceptance of demand deposits initially restricted to holding a maximum balance of Rs 100,000 per individual customer.

- Issuance of ATM/debit cards.

- They cannot issue credit cards.

- They are not allowed to give loans.

- Payments and remittance services through various channels.

- Distribution of non-risk sharing simple financial products like mutual fund units and insurance products, etc.

- They are only allowed to invest the money received from customers’ deposits into government securities.

- They cannot accept NRI deposits.

- A payments bank account holder would be able to deposit and withdraw money through any ATM or other service provider.

- Payments licensees would be granted to mobile firms, supermarket chains and others to cater to individuals and small businesses.

» Eligible Promoters of Payments Banks in India

- Existing non-bank Pre-paid Payment Instrument (PPI) issuers,

- Other entities such as individuals/professionals,

- Non-Banking Finance Companies (NBFCs),

- Corporate Business Correspondents (BCs), mobile telephone companies,

- Supermarket chains, companies, real sector cooperatives; that is owned and controlled by residents; and

- Public sector entities may apply to set up payments banks.

- A promoter/promoter group can have a joint venture with an existing scheduled commercial bank to set up a payments bank.

- Scheduled commercial banks can take an equity stake in a payments bank to the extent permitted under the Banking Regulation Act, 1949.

This is all from us in this article about the Payments Banks in India. We hope that you liked the information given in here. For more such informative articles, keep visiting Oliveboard.

If you are someone who is aspiring to become an RBI Grade B officer or a NABARD Grade A officer, we have online preparation courses for your comprehensive preparation. Have a look at the course offerings below.

II. NABARD Grade A Online Course

Check out Oliveboard’s Online Preparation Courses for NABARD Grade A exam comprising of Video Lessons, Study Notes, Current Affairs, Descriptive English, Topic Tests, Mock Tests for Phase-1, and Phase-2 and much more.Kick-start your Preparation with NABARD Grade A Cracker Course Here

What was the Objective behind Establishing Payments Bank?

Payments banks were established to boost financial inclusion, targeting the unbanked. Operating primarily through digital channels, they offer essential services, fostering accessibility and cost-effectiveness.

Key Objectives of Payments Banks:

- Financial Inclusion:

- The primary goal is to bring the unbanked and underbanked population into the formal financial system. Payments banks aim to provide banking services to individuals who may not have had access to traditional banks.

- Digital Transactions:

- Emphasis on digital transactions and electronic payments to foster a cashless economy. Payments banks leverage technology to provide convenient and secure digital banking experiences.

- Affordable Banking:

- To offer cost-effective and affordable banking services, with a focus on minimizing fees and transaction costs. This makes banking services more accessible to a broader spectrum of the population.

- Remote Access:

- Overcoming geographical barriers by providing banking services through digital channels, enabling individuals in remote areas to access basic financial services without the need for physical bank branches.

- Promoting Financial Literacy:

- Payments banks often engage in initiatives to enhance financial literacy, educating customers on the benefits of formal banking, digital transactions, and responsible financial management.

- Partnerships and Collaboration:

- Collaborating with existing banks, financial institutions, and technology providers to create a robust ecosystem for financial services. This involves leveraging partnerships to expand service offerings and reach.

III. RBI Grade B Online Course

Check out Oliveboard’s Online Preparation Courses for RBI Grade B comprising Video Lessons, Study Notes, Current Affairs, English Descriptive, Topic Tests, Mock Tests for Phase-1, Phase-2 (Objective + Descriptive Tests), and much more.Kick-start your Preparation with RBI Grade B Cracker CourseHere

Connect with us on

The most comprehensive online preparation portal for MBA, Banking and Government exams. Explore a range of mock tests and study material at www.oliveboard.in