Preparing for UPSC EPFO EO Exam 2021? If yes, then you are in the right place. Preparing for the exam requires you to cover a wide variety of subjects, covering each and every topic for the same.

Amidst the coronavirus outbreak, this is the best time to prepare for the UPSC EPFO EO 2021 and devote all your time to study. The candidates appearing for the exam must start their preparation, and here we are providing General Accounting Principles Notes For EPFO exam 2021. Have a look at the types of questions asked in the UPSC EPFO EO examination for free. Register here to take up practice questions.

1. General Accounting Principle Notes UPSC EPFO EO Exam 2021

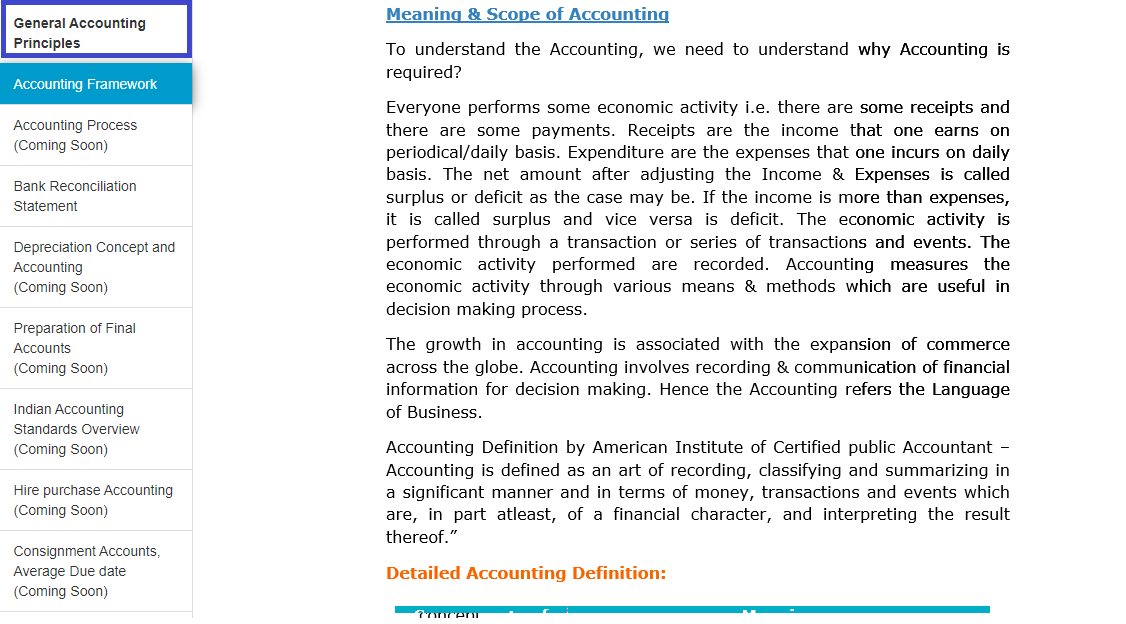

1.1 What is General Accounting Principle?

In order to maintain uniformity and consistency in accounting records, certain rules or principles have been developed which are generally accepted by the accounting profession. These rules are called by different names such as principles, concepts, conventions, postulates, assumptions, and modifying principles.

The term ‘principle’ has been defined by AICPA as ‘A general law or rule adopted or professed as a guide to action, a settled ground or basis of conduct or practice’. The word ‘generally’ means ‘in a general manner’, i.e. pertaining to many persons or cases or occasions. Thus, Generally Accepted Accounting Principles (GAAP) refers to the rules or guidelines adopted for recording and reporting of business transactions, in order to bring uniformity in the preparation and the presentation of financial statements.

Get Study Notes On UPSC EPFO EO Now! Click Here

2. Basic Accounting Concepts

The basic accounting concepts are referred to as the fundamental ideas or basic assumptions underlying the theory and practice of financial accounting and are broad working rules for all accounting activities and developed by the accounting profession. The important concepts have been listed below:

• Business entity.

• Money measurement.

• Going concern.

• Accounting period.

• Cost.

• Dual aspect (or Duality).

• Revenue recognition (Realisation).

• Matching.

• Full disclosure.

• Consistency.

• Conservatism (Prudence).

• Materiality.

• Objectivity.

Register Now & take Free Mock test To Assess Your preparations

2.1 Business entity

- The concept of business entity assumes that business has a distinct and separate entity from its owners. It means that for the purposes of accounting, the business and its owners are to be treated as two separate entities.

- Keeping this in view, when a person brings in some money as capital into his business, in accounting records, it is treated as a liability of the business to the owner.

- Here, one separate entity (owner) is assumed to be giving money to another distinct entity (business unit).

- Similarly, when the owner withdraws any money from the business for his personal expenses(drawings), it is treated as a reduction of the owner’s capital and consequently a reduction in the liabilities of the business.

2.2 Money Measurement

The concept of money measurement states that only those transactions and happenings in an organization that can be expressed in terms of money such as the sale of goods or payment of expenses or receipt of income, etc. are to be recorded in the book of accounts. All such transactions or happenings which can not be expressed in monetary terms, for example, the appointment of a manager, capabilities of its human resources or creativity of its research department or image of the organization among people, in general, do not find a place in the accounting records of a firm.

2.3 Going Concern Concept

The concept of going concern assumes that a business firm would continue to carry out its operations indefinitely, i.e. for a fairly long period of time and would not be liquidated in the foreseeable future. This is an important assumption of accounting as it provides the very basis for showing the value of assets in the balance sheet.

Get complete study notes on General Accounting and Principles here.

2.4 Accounting Period Concept

Accounting period refers to the span of time at the end of which the financial statements of an enterprise are prepared, to know whether it has earned profits or incurred losses during that period and what exactly is the position of its assets and liabilities at the end of that period. Such information is required by different users at regular intervals for various purposes, as no firm can wait for long to know its financial results as various decisions are to be taken at regular intervals on the basis of such information. The financial statements are, therefore, prepared at a regular interval, normally after a period of one year, so that timely information is made available to the users. This interval of time is called the accounting period.

2.5 Cost Concept

Under this cost concept, the value of the asset is determined based on historical cost i.e acquisition cost. The cost concept requires that all assets are recorded in the book of accounts at their purchase price, which includes the cost of acquisition, transportation, installation, and making the asset ready to use.

2.6 Dual Aspect Concept

The dual aspect is the foundation or basic principle of accounting. It provides the very basis for recording business transactions into the book of accounts. This concept states that every transaction has a dual or two-fold effect and should, therefore, be recorded in two places. In other words, at least two accounts will be involved in recording a transaction. This can be explained with the help of an example. Ram started the business by investing in a sum of Rs. 50,00,000 The amount of money brought in by Ram will result in an increase in the assets (cash) of business by Rs. 50,00,000. At the same time, the owner’s equity or capital will also increase by an equal amount. It may be seen that the two items that got affected by this transaction are cash and capital account.

2.7 Realization concept

Any change in the value of an asset is to be recorded only when the business realizes it. When an asset is recorded at its historical cost and even when its current costs increases, such change is not counted unless there is a certainty that such a change in material.

For complete study notes. Register here with your email id, password, and mobile no.

2.8 Matching Concept

The process of ascertaining the amount of profit earned or the loss incurred during a particular period involves the deduction of related expenses from the revenue earned during that period. The matching concept emphasizes exactly

this aspect. It states that expenses incurred in an accounting period should be matched with revenues during that period. It follows from this that the revenue and expenses incurred to earn these revenues must belong to the same accounting period.

2.9 Full Disclosure Concept

Information provided by financial statements is used by different groups of people such as investors, lenders, suppliers, and others in taking various financial decisions. In the corporate form of organization, there is a distinction between those managing the affairs of the enterprise and those owning it. Financial statements, however, are the only or basic means of communicating financial information to all interested parties. It becomes all the more important, therefore, that the financial statements make a full, fair, and adequate disclosure of all information that is relevant for making financial decisions.

2.10 Consistency Concept

The accounting information provided by the financial statements would be useful in drawing conclusions regarding the working of an enterprise only when it allows comparisons over a period of time as well as with the working of other enterprises. Thus, both inter-firm and inter-period comparisons are required to be made. This can be possible only when accounting policies and practices followed by enterprises are uniform and are consistent over the period of time.

2.11 Conservatism Concept

The concept of conservatism (also called ‘prudence’) provides guidance for recording transactions in the book of accounts and is based on the policy of playing safe. The concept states that a conscious approach should be adopted in ascertaining income so that the profits of the enterprise are not overstated. If the profits ascertained are more than the actual, it may lead to the distribution of dividends out of capital, which is not fair as it will lead to a reduction in the capital of the

enterprise.

You can find the summary notes here. Click Here & Register Yourself.

2.12 Materiality Concept

The concept of materiality requires that accounting should focus on material facts. Efforts should not be wasted in recording and presenting facts, which are immaterial in the determination of income. The question that arises here is

what is a material fact. The materiality of a fact depends on its nature and the amount involved.

2.13 Objectivity Concept

The concept of objectivity requires that accounting transactions should be recorded in an objective manner, free from the bias of accountants and others. This can be possible when each of the transactions is supported by verifiable

documents or vouchers. For example, the transaction for the purchase of materials may be supported by the cash receipt for the money paid, if the same is purchased on cash or copy of invoice and delivery challan, if the same is

purchased on credit. Similarly, the receipt for the amount paid for the purchase of a machine becomes the documentary evidence for the cost of the machine and provides an objective basis for verifying this transaction

3. UPSC EPFO EO Study Notes

1. 10 Mock Tests for EPFO EO in the latest pattern with detailed solutions

2. Summary Notes for all sections (except Quant, Eng)

- Indian Freedom Struggle (Click Here For Notes)

- Indian Polity and Economy (Click Here For Notes)

- General Accounting Principles (Click Here For Notes)

- Industrial Relations and Labor Laws (Click Here For Notes)

- General Science and Knowledge of Computer Applications (Click Here For Notes)

- Social Security in India (Click Here For Notes)

4. UPSC EPFO EO Study Material | Preparation Strategy

For topic-wise EPFO EO preparation strategy and preparation tips click on the blog link given below.

UPSC EPFO EO preparation strategy and preparation tips

This was all from us in this blog General Accounting Principle Notes UPSC EPFO EO Exam. Hope the information provided above will help you in your exam preparation. Stay tuned for more exam related information.

All The Best For Your Exam Preparation!

Also, Check:

Recommended Readings

- UPSC EPFO Topper’s Strategy, AIR 1’s Journery and Success Story

- UPSC EPFO Posting for EO/AO & APFC: Transfers & Growth

- UPSC EPFO Exam Date 2025, Admit Card Link for 230 Posts

- How to prepare Accounts and Auditing for UPSC EPFO Exam 2025?

- Preparation of Final Accounts: Meaning, Format & Objectives

- Accounting Standards: Meaning, Objectives, List & Importance

Hi, I’m Tripti, a senior content writer at Oliveboard, where I manage blog content along with community engagement across platforms like Telegram and WhatsApp. With 3+ years of experience in content and SEO optimization related to banking exams, I have led content for popular exams like SSC, banking, railway, and state exams.