RBI Repo Rate

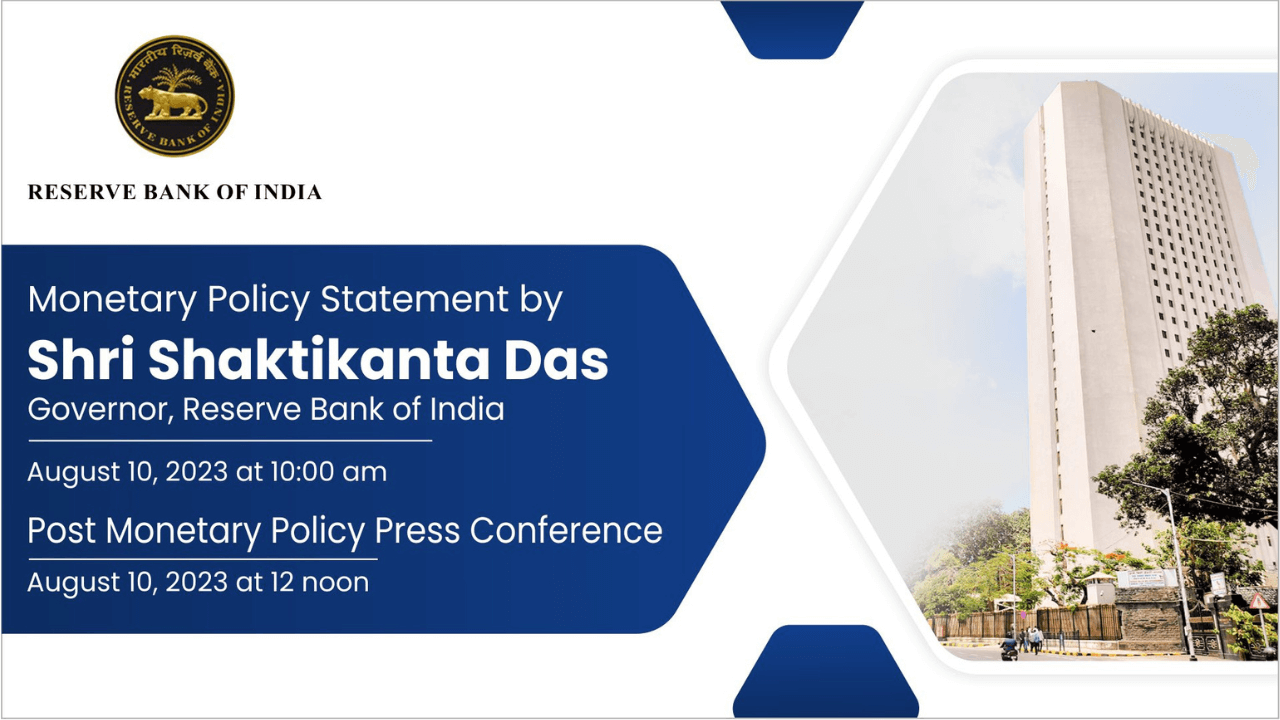

The Governor of the Reserve Bank of India (RBI), Shaktikanta Das, revealed the monetary policy for the third bi-monthly period of the fiscal year 2023-24. The Monetary Policy Committee (MPC), comprising six members, convened over a three-day period from August 8 to 10 to deliberate on these matters. In its announcement, the RBI has chosen to maintain the repo rate at its current level of 6.5%. This decision comes after a series of rate increases totaling 250 basis points (bps) since May 2022, reflecting the central bank’s approach to managing monetary conditions.

Key Highlights of the RBI Monetary Policy Committee (MPC)

Repo Rate

Following comprehensive discussions and careful consideration of various pertinent factors, the Monetary Policy Committee (MPC) arrived at a unanimous decision to maintain the policy repo rate under the liquidity adjustment facility (LAF) at its existing level of 6.50%.

Other Key Rates

- The standing deposit facility (SDF) rate will remain unchanged at 6.25%, while both the marginal standing facility (MSF) rate and the Bank Rate will remain at 6.75%.

- In a majority decision with five out of six members in agreement, the Monetary Policy Committee (MPC) has chosen to maintain its focus on gradually reducing accommodation to ensure that inflation aligns with the target over the medium term, while also providing support to economic growth.

These determinations are in line with the central objective of attaining the medium-term target for consumer price index (CPI) inflation of 4% within a tolerance range of +/- 2%, while concurrently fostering economic growth.

Global Growth

- Global economy facing challenges: elevated inflation, high debt, volatile financial conditions, geopolitical tensions, fragmentation, and extreme weather.

- Some economies are resilient, reducing hard landing fears.

- Global growth remains low despite IMF’s 2023 growth forecast increase.

- WTO predicts world trade volume growth to slow from 2.7% (2022) to 1.7% (2023).

- Uneven easing of headline inflation, major economies above target.

- The monetary tightening pace was reduced, but policy rates could stay high.

- Financial markets are volatile due to rating events, and incoming data, despite earlier optimism.

Domestic Growth

- India is expected to withstand external challenges better than many other countries.

- Positive momentum in overall economic activity, and uneven monsoon distribution.

- Industrial activity is steady, the services sector buoyant, and commercial vehicle sales and air cargo contracted.

- Buoyant urban and rural demand indicators, rising investment activity.

- Government capital expenditure, business optimism, private capex revival driving investment.

- Construction activity is strong, and capacity utilization in manufacturing is above the long-term average.

- The increased flow of resources to the commercial sector, merchandise exports, and services exports face challenges.

- Festival season and underlying developments to support consumption and investment.

- Real GDP growth is projected at 6.5% for 2023-24, with Q1 at 8.0%, Q2 at 6.5%, Q3 at 6.0%, and Q4 at 5.7%.

- Real GDP growth for Q1:2024-25 is projected at 6.6%, with even balanced risks.

Inflation

- The first quarter of the fiscal year 2023-24 saw headline inflation moderating to 4.6%, aligning with the forecasts set during the June MPC meeting.

- However, there was a slight uptick to 4.8% in June due to an increase in food inflation.

- On a positive note, core inflation, which excludes food and fuel, has decreased by over 100 basis points since its recent peak in January 2023.

- In July, food inflation intensified notably, mainly due to higher vegetable prices.

- The surge in tomato prices and continued price hikes in cereals and pulses contributed to this situation.

- Consequently, a significant rise in headline inflation is anticipated in the near future.

- The outlook for Kharif crops has improved due to better monsoon progress.

- Yet, uncertainties persist in the domestic food price outlook due to the potential impact of sudden weather events and the possibility of El Niño conditions in August and beyond.

Considering the ongoing uncertainties, our latest projections for CPI inflation in the fiscal year 2023-24, assuming a normal monsoon, have been revised to 5.4%, with the second quarter (Q2) at 6.2%, third quarter (Q3) at 5.7%, and fourth quarter (Q4) at 5.2%. The projected CPI inflation for the first quarter (Q1) of fiscal year 2024-25 stands at 5.2%. The associated risks are balanced evenly.

Liquidity and Financial Market Conditions

- Surplus liquidity increased due to the return of ₹2000 banknotes, RBI‘s surplus transfer, government spending, and capital inflows.

- Liquidity adjustment facility (LAF) daily absorption at ₹1.7 lakh crore in June and ₹1.8 lakh crore in July 2023.

- Market response to 14-day variable rate reverse repo (VRRR) auctions lukewarm, banks preferred standing deposit facility (SDF).

- Fine-tuning VRRR auctions of 1-4 days maturity had a better market response, reflecting risk aversion.

- The stated stance on liquidity is to maintain adequate liquidity for productive requirements, excess liquidity poses risks.

- Incremental cash reserve ratio (I-CRR) of 10% on increase in net demand and time liabilities (NDTL) from May 19 to July 28, 2023.

- I-CRR to absorb surplus liquidity, a temporary measure, to be reviewed on September 8, 2023, or earlier.

- The existing cash reserve ratio (CRR) is unchanged at 4.5%.

Financial Stability

- Indian financial sector is stable and resilient.

- Sustained growth in bank credit, low non-performing assets, adequate capital, and liquidity buffers.

- Macro stress tests show SCBs meet minimum capital requirements even under severe stress.

- No complacency, vulnerabilities can arise during tranquil times.

- Building buffers during stable periods is crucial.

- A stable financial system is essential for price stability and sustained growth.

- Shared responsibility with regulated entities (banks, NBFCs) as important stakeholders.

- RBI is committed to safeguarding the financial system from emerging challenges.

- Expect regulated entities to share the commitment.

External Sector

- CAD contained 2.0% of GDP in 2022-23 from 1.2% in 2021-22.

- Q1 of 2023-24 sees narrowed merchandise trade deficit due to more import contraction than exports.

- Services exports and remittances are expected to cushion CAD.

- FPI flows robust, net FPI inflows highest since 2014-15 at US$ 20.1 billion.

- External commercial borrowings show net inflows of US$ 6.0 billion in April-June 2023.

- Net FDI flows declined to US$ 5.5 billion in April-May 2023 due to the global FDI slowdown.

- The external debt to GDP ratio improved to 18.9% at end-March 2023.

- Indian rupee stable since January 2023.

- Foreign exchange reserves cross US$ 600 billion.

- Positive economic indicators reflect a strong financial position.

- 16th to 22nd July 2026 Weekly Current Affairs PDF & Quiz

- States and Capitals of India: Total States, Capitals, Chief Ministers and Governors

- How many months of Current Affairs are required for bank mains?

- Weekly Current Affairs 8th to 15th July 2026, FREE PDF & Quiz

- Weekly Current Affairs 2026 for Bank, SSC, Railways & PCS Exams

- Monthly Current Affairs 2026 PDF For SSC, Banking, and Railways

Hello, I’m Aditi, the creative mind behind the words at Oliveboard. As a content writer specializing in state-level exams, my mission is to unravel the complexities of exam information, ensuring aspiring candidates find clarity and confidence. Having walked the path of an aspirant myself, I bring a unique perspective to my work, crafting accessible content on Exam Notifications, Admit Cards, and Results.

At Oliveboard, I play a crucial role in empowering candidates throughout their exam journey. My dedication lies in making the seemingly daunting process not only understandable but also rewarding. Join me as I break down barriers in exam preparation, providing timely insights and valuable resources. Let’s navigate the path to success together, one well-informed step at a time.