Different Types of Borrowers: In economy, all transactions have at least two parties. These are- the lender/seller, the borrower/buyer. When it comes to banks, the number and type of borrowers are largely varied The can be private firms, individuals, trust funds, public limited companies, huge corporations, public sector undertakings, multinational corporations, etc. All of these may borrow for various reasons.

This ebook will cover the different type of debtors, the types of borrowers than come under these sections, the requirements from each type of borrower, and other important points relating to borrowers.

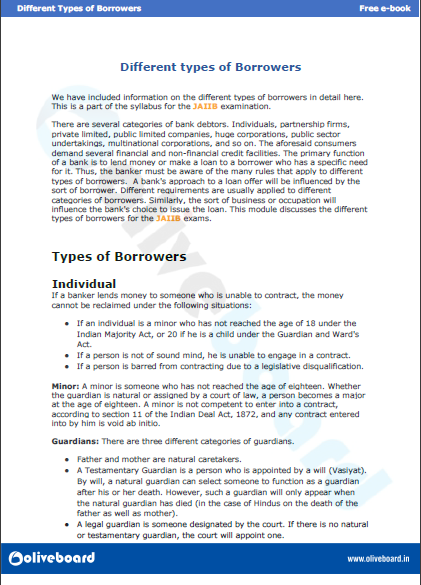

Different Types Borrowers

Different Types Borrowers: Individual

If a banker lends money to someone who is unable to contract, the money cannot be saught back under the following situations:

- If an individual is a minor who has not reached the age of 18 under the Indian Majority Act, or 20 if he is a child under the Guardian and Ward’s Act.

- If a person is not of sound mind, he is unable to engage in a contract.

- If a person is barred from contracting due to a legislative disqualification.

Minor: A minor is someone who has not reached the age of eighteen. Whether the guardian is natural or assigned by a court of law, a person becomes a major at the age of eighteen. A minor is not competent to enter into a contract, according to section 11 of the Indian Deal Act, 1872, and any contract entered into by him is void ab initio.

Guardians: There are three different categories of guardian

- Father and mother are natural caretakers.

- By will (Vasiyat), a natural guardian can select someone to function as a guardian after his or her death. Such a guardian is a Tetsamentary Guardian. However, such a guardian will only appear when the natural guardian has died (in the case of Hindus on the death of the father as well as mother).

- When the court designates a guardian, they become a legal guardian. If there is no natural or testamentary guardian, the court will appoint one.Different T ypes of B orrowers

When a Hindu minor’s guardian stops being a Hindu or becomes a sanyasi, he loses his status as a natural guardian.

Different Types Borrowers: Partnership Firms

- The Indian Partnership Act of 1932 governs partnerships. A contract establishes a partnership.

- A partnership helps manage a profitable business.

Legal Status of Partnership

According to the Indian Partnership Act of 1932, which governs partnerships, a lender dealing with a partnership firm must confirm whether the firm is registered or not.

- Section 19 of the Partnership Act, 1932 addresses the implied authority of a partner as an agent of the firm, whereas Section 22 addresses the way of executing actions to bind the partnership.

- The minimum number of partners is two, with a maximum of ten for banking and twenty for other businesses.

- Who is eligible to become a partner: A single person, a partnership, or a limited business.

- Who is not eligible for partnership: Minors, insolvents, and insane people are unable to become partners because they lack the legal capacity to contract.

- A minor cannot become a partner, but he can claim his share in the profits.

- According to a Supreme Court judgement, HUFs cannot become partners since they are not accountable for the actions of others.

- A trust cannot become a partner as partners are better for business

- The registrar of businesses registers a partnership firm.

- It is not necessary to register a partnership firm. It is not essential to register the company. However, an unregistered firm cannot sue others for the collection of its debt, but others can sue the firm.

Partner’s liability

During his or her time as a partner, each partner is jointly and individually accountable for all activities of the company. His legal responsibility is limitless.and all previous checks issued by the insolvent partner must be paid if the partner confirms the same.

Insolvency of a Partner:

The other partner can easily continue to operate the fiirm in case of insolvency when the firm’s account is in credit. However, the banker muct obtain a new mandate and all previous checks from the insolvent parrner must be paid if the partner confirms the same.

Operational Authority: In partnership accounts, all partners have operational power.

- Any change in operational power requires the approval of all partners.

- Every partner, including a sleeping partner, can halt payment of a cheque signed by another partner of the firm, although revocation may only be done by the operational authority.

- Partner is unable to delegate authority.

- Death Of A Partner: Because the death of a partner dissolves the Partnership firm, banks are obligated to cease the firm’s transactions in a running credit facility such as Cash credit and enable the transaction in a separate bank account so that the firm’s operation is not harmed.

- The remaining partners’ approval will be obtained before the cheques signed by the deceased, insane, or insolvent partner are paid.

- If the partner’s account is in credit, operations are permitted for the firm’s closure.

- If the account is in debit, activities should be halted to preserve the obligation of the deceased/insolvent partner or his/her estate and to prevent Clayton’s rule operations.

Different Types Borrowers: Hindu Undivided Family

- A banker working with a Hindu Undivided Family should be familiar with the ‘Karta,’ the family’s senior member.

- The banker should guarantee that the family ‘Karta’ does business with the bank and only borrows for the benefit of the family company.

- All members must sign the application to start an account, and all adult members should sign it together.

- HUF is neither a legal entity nor an individual. It is not the result of an agreement.

- It is not a legal entity. Membership is through birth or adoption and is based on a shared ancestor.

- The Karta is the family’s oldest member, and the others are co-parents.

- Karta might also be a daughter.

- Even if he or she resides outside of India, Karta remains the most senior member.

- The account’s operational power is in the hands of Karta

- Karts has the authority to designate any other coparcener or third party to perform HUF transactions and/or manage the accoun. A co-partner cannot halt the payment of cheque.

- A co parcener’s responsibility is limited to his stake in the company. He is not directly accountable.

- According to a Supreme Court ruling, HUF cannot be a partner.

A joint family’s manager or ‘Karta’ has the certain powers and duties:

Power

- Possession and administration of joint family property are both rights.

- Right to a share of the revenue from a joint family property

- Right to speak for the entire family

- Right to sell joint family property for a specific reason

Duties

- The responsibility of running the family company and managing the property for the family’s benefit.

- Accountability for revenue and property from a shared family company.

Different Types Borrowers: Companies

A company is another kind of borrower that a banker interacts with within his lending business.

Basic laws governing companies: Companies in India are presently governed under the Companies Act, 2013. Companies are needed to be registered under the Companies Act of 1956. Section 11 of the Companies Act of 1956 states that an organisation or partnership with more than ten members in the event of a banking company and more than twenty members in the case of other business.

Incorporation of Company: Section 12 of the Companies Act of 1956 states that any seven or more people or where a business is known are known by two documents called “Memorandum of Association” and “Articles of Association.”

- Memorandum of Association: It provides the name of the company, registered office, its authorised capital, shareholders’ liabilities, and the firm’s purposes, among other things.

- Articles of Association: These are the rules and regulations that regulate the company’s internal management. For example, the number of directors, the company’s borrowing powers, the procedure for transferring and transmitting shares, and so on.

Statutory Corporations

Companies are registered under the Companies Act of 1956, and corporations may be constituted by an Act of Parliament. These are referred to as Statutory Corporations. The State Bank of India, for example, was created under the State Bank Act of 1955. Statutory corporations are independent corporate organisations established by a special Act of Parliament or a state legislature, with specific functions, duties, powers, and immunities outlined in the Act of the legislature. Statutory companies have financial autonomy and are accountable to the legislation under which they were founded.

Features:

The following are the primary characteristics of the statutory corporation:

- Corporate Body: It is a legal entity and an artificial person formed by law. The government appoints a board of directors to administer such businesses. A corporation has the authority to engage in contracts and do business in its name.

- State-owned: The state assists such firms by totally or partially contributing to their capital. The state owns it entirely.

- Answerable to the Legislature: A statutory company is accountable to the legislature or state assembly that established it. Parliament has no authority to meddle with statutory corporations’ operations. It can only address policy issues and corporate performance.

- Own Staffing System: Employees are not government employees, even though the government owns and oversees a firm. The government provides balanced or consistent pay and benefits to employees of diverse firms. They are hired, compensated, and regulated by the corporation’s regulations.

- Financial Independence: A statutory company has financial independence or autonomy. It is exempt from the budget, accounting, and audit controls. It can even borrow funds within and outside the country with prior approval from the government.

Different Types Borrowers: Trusts

- The Indian Trust Act of 1882 governs trusts. A banker who deals with trusts should be familiar with the laws that apply to them.

- The responsibilities and obligations of the trustee set down in the trust deed come under laws that apply to such trusts.

- When dealing with a trust, the banker should make sure to have all of the necessary permissions from the appropriate government agencies.

- Private trusts have beneficiaries who are specific persons or groups, whereas public trusts have beneficiaries who are the general public.

- Indian Trust Act of 1882 governs Private Trusts, while the states’s Public Trust Act oversees the Public Trusts. The Charity Commissioner oversees the registration of public trusts.

- The Trust Deed must carry out the bank account’s operation and other features. If the trust deed does not specify operational power, all trustees must jointly manage the account.

- Operational Authorities control payment. Operational Authorities have lifted stop payment.

- Even by unanimous consent, trustees cannot assign their authority to an outsider.

- Banks approve loans to Trusts if the loans are permissable under the Trust Deed, and are for the benefit of the Trust.

- When a trustee dies, the trust property goes on to the next trustee, although the court can choose a trustee if the lone trustee or last living trustee dies.

- Trustee’s death or insolvency does not affect the Trust property and the bank can cash cheques made by a dead trustee before his his death.

Different Types Borrowers: Clubs & Societies

- Clubs, schools and non-commercial organisations do not come under the laws that non-commercial organisations that do not come under under the laws that govern them cannot transact. s Act or Co-operative Societies Act normally control these organisations.

- The bank will require a Certificate of Registration, the Society’s Byelaws, and a decision from the Managing or Executive Committee to create a Clubs and Societies account.

- The Managing Committee will decide on operational authority.

- The Managing Committee has decided to change the operational authority.

- Operational Authority’s stop payment and reversal of stop payment.

- If everything else is in order, a cheque signed by the treasurer, secretary, or president of the society and given after his death can be paid.

Take A Sneak Peek At the Different Types of Borrrowers eBook for JAIIB

Download the Different Types of Borrowers Free eBook for JAIIB

How to Download Different Types of Borrowers Free eBook for JAIIB?

Step 1: Click on the download link. You will be redirected to Oliveboard’s FREE E-Books Page.

Step 2: Create a free Oliveboard account or login using your existing Oliveboard account details

Step 3: Download the book by clicking on the link presented on the page.

Recommended Reading:

- JAIIB Exam Analysis 2022 I Paper 2 – AFB I Feb 2022

- JAIIB Exam Analysis 2022 I Paper 1 – PPB I Feb 2022

- Preparation Tips for JAIIB Exam- Last Minute Strategy

- JAIIB Revision Plan- Last 10 Days Plan

- JAIIB Frequently Asked Questions- 2022| Check Here (oliveboard.in)

- JAIIB Genius | JAIIB Weekly Quiz PDF – JAIIB Questions PDF (oliveboard.in)

- JAIIB Full Form – Junior Associate of the Indian Institute of Bankers (oliveboard.in)

- JAIIB and CAIIB Books- Exams Syllabus, Books, and more (oliveboard.in)

Also Check:

- JAIIB 2022 Exam -Notification Released (oliveboard.in)

- JAIIB Notification 2022 – Notification PDF, Eligibility, (oliveboard.in)

- JAIIB Apply Online – Application Form 2022, Fees, Instru (oliveboard.in)

- JAIIB Eligibility – Age, Degree, Nationality, Members (oliveboard.in)

- JAIIB Syllabus – Complete List of Papers, Modules (oliveboard.in)

- JAIIB Exam Pattern 2022 – Details of Pattern, Marking (oliveboard.in)

- JAIIB Admit Card November 2022 – Steps and Direct Download (oliveboard.in)

- JAIIB 2022 Cut Offs – Check JAIIB Minimum Cut Off (oliveboard.in)