The primary role of the bank is to keep people’s money safe and to make loans to those who need them. People deposit money with banks, which the banks then use to provide loans to other people. Aside from these primary duties, banks also conduct a variety of other activities. Increased competition in the banking industry, technical developments, and a variety of other factors all led to the rise of products and services. As a professional banker you will be expected to know the functions of banks and other basics. So in this blog you will learn about Functions of bank- Relationships, Norms & Others. You can download Functions of Bank- Relationships, Norms & Others free e-book.

How to Download the Functions of Bank- Relationships, Norms & Others Free Ebook

How to Download The Functions of Bank- Relationships, Norms & Others E-book for JAIIB?

Step 1: Click on the download link. You will be redirected to Oliveboard’s FREE E-Books Page.

Step 2: Create a free Oliveboard account or login using your existing Oliveboard account details

Step 3: Download the book by clicking on the link presented on the page.

Introduction

Functions of Bank

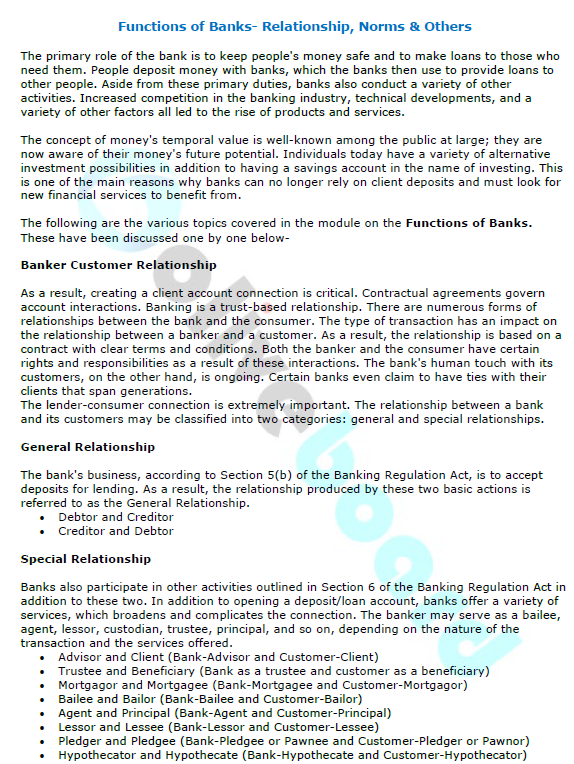

The primary role of the bank is to keep people’s money safe and to make loans to those who need them. People deposit money with banks, which the banks then use to provide loans to other people. Aside from these primary duties, banks also conduct a variety of other activities. Increased competition in the banking industry, technical developments, and a variety of other factors all led to the rise of products and services.

The concept of money’s temporal value is well-known among the public at large; they are now aware of their money’s future potential. Individuals today have a variety of alternative investment possibilities in addition to having a savings account in the name of investing. This is one of the main reasons why banks can no longer rely on client deposits and must look for new financial services to benefit from.

The following are the various topics covered in the module on the Functions of Banks. These have been discussed one by one below-

Banker Customer Relationship

As a result, creating a client account connection is critical. Contractual agreements govern account interactions. Banking is a trust-based relationship. There are numerous forms of relationships between the bank and the consumer. The type of transaction has an impact on the relationship between a banker and a customer. As a result, the relationship is based on a contract with clear terms and conditions. Both the banker and the consumer have certain rights and responsibilities as a result of these interactions. The bank’s human touch with its customers, on the other hand, is ongoing. Certain banks even claim to have ties with their clients that span generations.

The lender-consumer connection is extremely important. The relationship between a bank and its customers may be classified into two categories: general and special relationships.

General Relationship

The bank’s business, according to Section 5(b) of the Banking Regulation Act, is to accept deposits for lending. As a result, the relationship produced by these two basic actions is referred to as the General Relationship.

- Debtor and Creditor

- Creditor and Debtor

Special Relationship

Banks also participate in other activities outlined in Section 6 of the Banking Regulation Act in addition to these two. In addition to opening a deposit/loan account, banks offer a variety of services, which broadens and complicates the connection. The banker may serve as a bailee, agent, lessor, custodian, trustee, principal, and so on, depending on the nature of the transaction and the services offered.

- Advisor and Client (Bank-Advisor and Customer-Client)

- Trustee and Beneficiary( Bank as a trustee and customer as a beneficiary)

- Mortgagor and Mortgagee (Bank-Mortgagee and Customer-Mortgagor)

- Bailee and Bailor (Bank-Bailee and Customer-Bailor)

- Agent and Principal (Bank-Agent and Customer-Principal)

- Lessor and Lessee (Bank-Lessor and Customer-Lessee)

- Pledger and Pledgee (Bank-Pledgee or Pawnee and Customer-Pledger or Pawnor)

- Hypothecator and Hypothecatee (Bank-Hypothecatee and Customer-Hypothecator)

- Indemnity holder and Indemnifier (Bank-Indemnity Holder and Customer-Indemnifier)

- As a Guarantor

- As a Custodian

KYC/CFT/AML Norms

- KYC criteria were implemented to ensure combating terrorist financing (CTF), anti-money laundering (AML), and risk management.

- Customer Identification Procedures, Risk Management, Customer Acceptance Policy, and Transaction Monitoring are the four important features that banks must incorporate into their KYC policies.

- Banks are required to collect the client’s identity and address at the moment the consumer opens a bank account.

- Consumers are divided into three groups: high-risk customers, medium-risk customers, and low-risk customers.

- Pensioners, government departments, salaried individuals, and no-frills accounts are examples of low-risk consumers.

- High-risk consumers include HNWIs, trusts, NGOs, politically exposed individuals, and so on.

- Banks should examine their clients’ risk profiles at least once every six months.

- Customer identifying data and entire KYC exercises should be updated regularly as follows:

- Low Risk – Every 10 years

- Medium Risk- Every 8 years

- High Risk- Every 2 years

Take Sneak Peek at Functions of Bank-Relationship, Norms & Others E-book

Conclusion

We hope this e-book provides you with detailed knowledge regarding the JAIIB Exam Functions of Bank-Relationship, Norms & Others. Please contact Oliveboard if you have any questions.

Keep following Oliveboard for more updates. To stay updated, follow Oliveboard on Facebook and Telegram.

FAQs

A. A farmer’s credit requirements are addressed by two types of agricultural advances: direct and indirect financing. Direct finance is classified into two types: short-term loans and medium- to long-term loans. Farmers can get direct agricultural finance for short-term demands like crop production as well as medium- and long-term needs like land expansion and water resource enhancement.

A. A cheque is a bill of exchange that is always payable on demand and always has a banker as the drawee. It also incorporates truncated and electronic cheques.

JAIIB Study Material Compilation

Also Read:

- Preparation Tips for JAIIB Exam- Last Minute Strategy

- JAIIB Revision Plan- Last 10 Days Plan

- JAIIB Frequently Asked Questions- 2022| Check Here (oliveboard.in)

- JAIIB Genius | JAIIB Weekly Quiz PDF – JAIIB Questions PDF (oliveboard.in)

- JAIIB Full Form – Junior Associate of the Indian Institute of Bankers (oliveboard.in)

- JAIIB and CAIIB Books- Exams Syllabus, Books, and more (oliveboard.in)

Also Check:

- JAIIB 2022 Exam -Notification Released (oliveboard.in)

- JAIIB Notification 2022 – Notification PDF, Eligibility, (oliveboard.in)

- JAIIB Apply Online – Application Form 2022, Fees, Instru (oliveboard.in)

- JAIIB Eligibility – Age, Degree, Nationality, Members (oliveboard.in)

- JAIIB Syllabus – Complete List of Papers, Modules (oliveboard.in)

- JAIIB Exam Pattern 2022 – Details of Pattern, Marking (oliveboard.in)

- JAIIB Admit Card November 2022 – Steps and Direct Download (oliveboard.in)

- JAIIB 2022 Cut Offs – Check JAIIB Minimum Cut Off (oliveboard.in)

Oliveboard Live Courses & Mock Test Series

- RBI Assistant 2022 – Attempt Free Mains Mock Test

- ESIC UDC Mock Test – Attempt A Free Mains Test Here

- ECGC PO Mock Test – Attempt a Free Test Here

- SSC CGL 2021 Tier 1 – Attempt Free Actual Exam Pattern Test Here

- SIDBI Mock Test – Attempt Now

Hello there! I’m a dedicated Government Job aspirant turned passionate writer & content marketer. My blogs are a one-stop destination for accurate and comprehensive information on exam categories like Regulatory Bodies, Banking, SSC, State PSCs, and more. I am on a mission to provide you with all the details you need, conveniently in one place. When I am not writing and marketing, you will find me happily experimenting in the kitchen, cooking up delightful treats. Join me on this journey of knowledge and flavors!